Segmenting Healthcare Innovation

Clinical, operational and commercial innovations offer distinct investment profiles

Early-stage investing funds innovation to create and capture economic value.

In healthcare, I see a few distinct categories of innovation, each with a unique risk/return profile that informs everything from investment sourcing to portfolio construction.

The Standard of Care

At the risk of oversimplifying for brevity, I will define the healthcare market as the goods and services of the standard of care, where the “standard of care” is how medical issues are treated.

In this context, we can say that the contours of the healthcare market are shaped by:

What the standard of care is (clinical)

How the standard of care is delivered (operational)

How the standard of care is paid for (commercial)

These buckets create a framework to classify innovations. The chart below illustrates how I think about risk and return across these categories.

It’s not perfect, but this framework helps me screen and assess investment opportunities. My current investment mandate favors a high-conviction, concentrated portfolio of assets with asymmetric upside on low capital intensity (i.e. doesn’t require a massive amount of capital to scale). It also favors flexible liquidity, prioritizing exit optionality and avoiding write-offs over pure “unicorn” potential (i.e. not every company needs to be a “grand-slam”).

With this mandate, I’m drawn to commercial innovations and niche operational innovations, for reasons I’ll explain below.

As always, I would love to hear your feedback because this framework is something I plan to calibrate over time.

Clinical Innovation

What is it: Clinical innovation changes what the standard of care is. Clinical innovations advance the prevailing set of methods by which medical conditions are treated. In short, they change the “medicine” itself.

Examples: In this context, “medicine” is the combination of diagnostics and clinical interventions to treat issues. This would include diagnostics, biopharma products, medical devices, surgical interventions, and other direct treatment modalities. I would also include technologies that support the direct delivery of those diagnostics and interventions.

Risk Profile: First, clinical innovations have a baseline scientific “does it work?” risk. Companies must show that clinical innovations “work” via hard research. Getting through this research phase (e.g. FDA approval process for biopharma products) is hard. Most attempts fail — e.g. the average success rate for new pharma products is <10%.

This expensive, low-hit-rate research makes clinical innovations extremely capital intensive. Importantly, this capital intensity comes long before there's any certainty of commercial viability. Regulatory outcomes are generally binary - clinical innovations either outperform the status quo or they don’t.

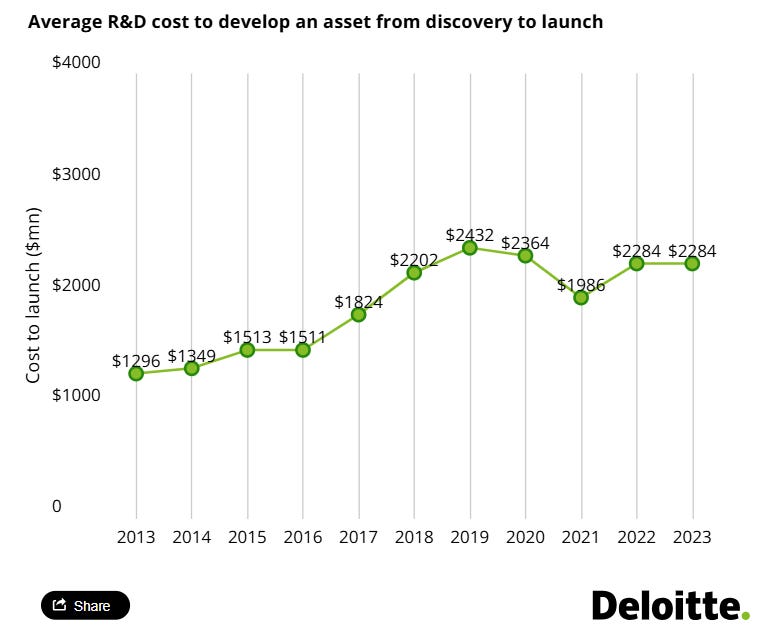

These dynamics explain why the cost to bring a new drug to market exceeds $1bn.

Theoretically, once you have proven that the “new thing” is sufficiently better than the “old thing,” commercializing the new thing should be easy. There should be no reason for a doctor to prescribe the inferior, old thing.

Further, because clinical innovations typically have robust patent protections, theoretically there’s no competition for your new thing for a definite period of time. This should enable clinical innovations to capture massive market value unencumbered.

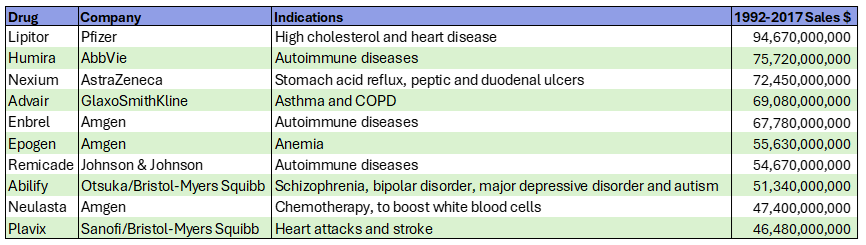

Sure enough, these market dynamics have enabled multiple blockbuster drugs to achieve billions in lifetime revenues.

In practice, however, there are many hurdles to the pot of gold at the end of the regulatory rainbow.

First, the payment model for biopharma products and medical devices is highly convoluted. This creates reimbursement risk. For example, pharma companies have to convince insurance companies that paying for their innovations will deliver a compelling ROI.

Also, doctors and patients need to be educated about the product. There is real commercial execution risk involved in things like engaging key opinion leaders and establishing distribution channels.

Still, in broad strokes, we can say that if a clinical innovation “hits”, the financial outcome is massive.

Portfolio Implications: This results in a boom-or-bust risk/return profile for clinical innovations.

Successful investing is based on deploying capital with a margin of safety. In venture capital, you can either build that margin of safety into the disciplined pricing/structure at the asset level (value investing, at the extreme) or diversification at the portfolio level (“spray-and-pray,” at the extreme).

But there is no real way to de-risk a clinical innovation at the asset level; even with the perfect team, the fundamental “does it work” risk can only be resolved by the research.

At the same time, these companies offer “return the fund” outcome potential. Given this dynamic, successful clinical innovation investing requires a diversified portfolio rather than a concentrated portfolio.

I avoid clinical innovations because of the capital intensity and binary regulatory risk, which doesn’t fit with the concentrated portfolio construction of the strategy I’m on. And also because I am just a dumb excel monkey who gets queasy around blood and chemistry.

Still, I deeply admire investors and operators in this category — clinical innovations are ultimately the biggest drivers of progress in human health.

Operational Innovation

What is it: Operational innovation changes the way that the standard of care is delivered and administered.

Examples: This is the broadest category, encompassing most services and software businesses that attack the massive administrative layer in healthcare.

This category includes provider-focused innovations (e.g. documentation tools, clinical decision support, prior authorization automation) and payor-focused innovations (e.g. population health analytics, utilization management).

There might be some patient-focused innovations too, but because patients are not usually the “buyer” for healthcare innovations, the scope for creating and capturing value from patients directly is limited.

Risk Profile: Operational innovations have significantly less “does it work” risk. Companies can quickly assess whether a new software or services model is going to work in a binary sense, even before generating revenue. The remaining “does it work” risk is based on how much ROI/impact the innovation delivers, which can typically be measured once early customers adopt the offering.

Unfortunately, having less “does it work” risk is a double-edged sword. It lowers the barriers of entry, which means that you can get to market faster, but there is also more competition.

A central challenge with operational innovations in healthcare is that the problem areas with the big TAM opportunities are generally well-known — e.g. documentation, billing, coding, prior authorizations, etc.

A common market pattern when there is a new technology is that a lot of people think — hey, let’s take the new technology and apply it to the known problem with a big TAM. When there are low barriers to entry and limited points of differentiation, this leads to rapid saturation of new categories.

We’re seeing this now with the proliferation of AI companies attacking the same opportunity sets — like the >50 “ambient AI scribe” companies in the market.

The low barriers to entry create go-to-market complexity, which drives capital intensity. Companies must spend more to sell in a crowded market and invest heavily in R&D to stay ahead of competitors. As a result, operational innovation categories can easily turn into arms races where players are incentivized to raise massive war chests in a bid to “win” the market.

Complexity is a lever for operational innovations to build a competitive moat. Absorbing complexity from the customer enhances stickiness and differentiation. This often drives services and software models to converge. Services companies often need to invest in infrastructure and technology in order to absorb more complexity at scale. Software companies often need to invest in a services layer in order to ensure customers rapidly and sustainably realize ROI.

An important consideration in assessing the commercial viability of an operational innovation is to look at where on the customer’s P&L the innovation delivers an impact. Specifically, does the innovation a) increase revenues or b) reduce costs?

Operational innovations that increase revenue are almost always more compelling. There’s less friction involved in making the revenue printer go BRRR. Cost reductions, which typically involve reducing headcount or obviating vendor spend, elicit more resistance through the sales cycle.

Portfolio Implications: Operational innovations can be really compelling for a more concentrated investment strategy if there is a meaningful, durable differentiation — either differentiation built into the offering (e.g. complexity approach) or in the market focus (e.g. overlooked niche positioning).

Operational innovations are highly dependent on execution. That means investors in this category need to be comfortable leaning in to help entrepreneurs scale. For example, in an operational innovation business, things like making the first head of sales hire and developing the right sales commission structure are super important. Investors who have the ability and appetite to assist founders in thinking through execution at that tactical level are better positioned for success. This dynamic fits well with a concentrated portfolio because there’s less dilution of time/resources/bandwidth.

So while I am scared of the “arms race” categories with low barriers to entry and limited differentiation, companies that build differentiation through a niche focus or complexity can be very interesting for high-conviction portfolios.

Commercial Innovation

What is it: Commercial innovation changes the way that the standard of care is paid for. Often, these are business model innovations that work to align stakeholders in the value chain, while capturing a significant financial spread or revenue opportunity.

Examples: Value-based or risk-based business models. Most value-based care companies boil down to doing some clinical intervention or activity really well and using the improved outcomes to create and capture a financial spread.

Another category I would lump in here is marketplace businesses that transform how specific aspects of healthcare are transacted (e.g. rentable clinician networks). I’d also include companies here that have developed unique go-to-market approaches wherein they absorb risk to make it easier for a customer to say “yes.” As an illustration, TapestryHealth (Sopris portfolio company) takes on some financial risk of installing hardware for skilled-nursing facilities in order to reduce the friction for adoption to customers.

Risk Profile: The major risk for commercial innovations is making sure the rails of the “mousetrap” are set up correctly and that the Company can actually deliver on the risk it assumes. Once you know it “works,” then scaling via more volume/risk is relatively straightforward. Because these models often absorb risk from customers, there is a clear value proposition and less sales friction. This means less overall go-to-market execution risk.

Portfolio Implications: Companies with a novel commercial innovation tend to be the most rare. Creating a new way to transact requires a diverse skill set, more so than other categories of healthcare. For example, a fee-for-service care delivery company needs to excel at care delivery. Meanwhile, a risk-based model requires actuarial and contract design expertise. With each additional layer of complexity in a commercial innovation, the founding team needs a wider range of experience to be successful. The scarcity of these assets is an important portfolio construction consideration — it would be difficult to build a large portfolio constructed solely of commercial innovations. But for a concentrated investment mandate, the scarcity is less concerning.

From an outcomes standpoint, this category offers robust exposure to asymmetric upside. Once you know it “works,” commercial innovations can scale in a rapid, continuous motion. While clinical innovations also offer step-function value upside, they require orders of magnitude more capital. Commercial innovations are more attractive from a dollars-in to dollars-out standpoint. One caveat: models that function like quasi-insurance companies may face capitalization complexity if there is a need for an insurance-like balance sheet reserve (e.g. if they are subject to downside risk).

🧨🧨 Short-Fuse Asymmetric Upside Investing

Ultimately, I find the categories of niche operational innovations and risk-based commercial innovations to be the most compelling. They offer faster feedback loops to commercial viability and lower commercial intensity (less competition). They’re hard to find, but they offer really attractive asymmetric upside with optionality that fits well with a concentrated, durable, returns-oriented early-stage portfolio.

So if you’re working on something like this, hit my line asap!!